SG Super contributions set to increase July 2021 to 10% and will increase each year by 0.5% until 2026

Now, this is only 0.5% of what our current Super guarantee is (which is 9.5%), not much right? Well, I guess that really depends on how much you are earning, and this can make a BIG differencein the long run.

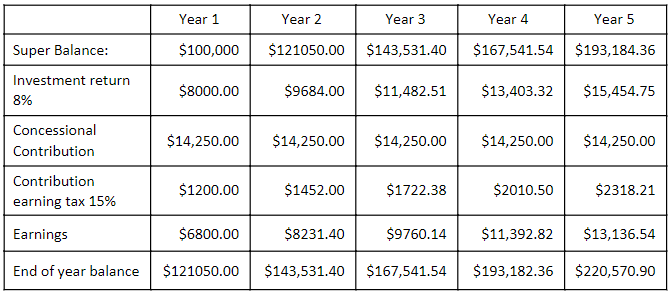

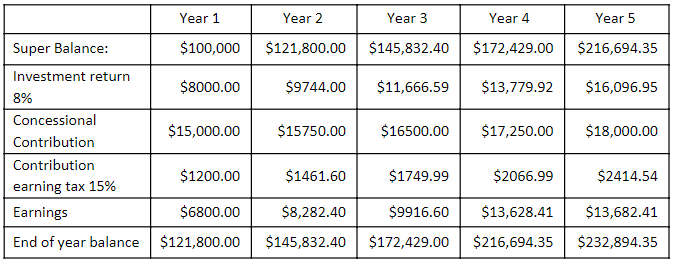

For example, if you are earning $150,000.00 gross you would be putting away $14,250.00 at the current 9.5%, however if you are putting 10% away it would be $15,000.00, that added $750.00 invested each year with compounding interest of 8% over a 5-year period would equate to $4751.95 extra…

The good news is that the government plan on increasing our Super Guarantee contributions over 5 years beginning this financial year of 2021.

So, let me demonstrate in the table below how this will look for your super and why this is a positive move for us all:

Before the increase:

After the increase:

Ok, now you can see the snowball effect this compounding interest has plus increased SG contributions you can imagine how fast this is going in increase over the next 5 years.

Let us not stop there…. If you are in your 40s or over, you are now looking down the barrel toward retirement so to give your super a greater boost you can do a few more things that will add to your wealth creation.

Salary sacrifice:

You can make additional concessional contributions (before tax) up to $25,000 each year – be mindful of what you have already paid via you super guarantee with your employer. If you have a consistent salary then it will be easy to set a salary sacrifice arrangement with your payroll. Another option is to make a concessional contribution before the end of the financial year once you know what you have already contributed and add more (again up to $25K). You can then declare this added contribution as a concessional contribution with your chosen fund and get a tax deduction.

Non-concessional contributions:

This is a great way to boost your retirement savings. Often, we save money and invest outside of super not giving our retirement savings any thought. If you do make this kind of contribution you are paying with money you have already paid tax on. What this means is when invested in your super you won’t be paying any tax… yes, that’s right NO tax. Apart from our residential property this is the only other tax-free investment you can have. Of course, there are rules, you can only contribute up to $100,000 per year, however there are a few cases where you can add more – for example you can use the down sizer rule when if you were to sell your family home, or the Bring it forward rule. I will go into more detail on these strategies – along with additional super strategies in the coming weeks.

Please also consider your personal circumstances. Often people don’t put money in super as it then locked away, but if you have paid down your mortgage and/or have surplus income to put toward your future then I recommend you seek advice and get a strategy in place that can set you up toward a comfortable retirement.

*investment returns are based on average returns of balanced investments and will fluctuate from year to year, we used 8% to demonstrate how investing and the compounding effect has on an investment over a long-term period.

This is information is general in nature and has not considered your personal circumstances. Please seek financial advice from a licensed adviser.